Texas Builders Risk Insurance

Your building is covered. The soft costs decide what a delay costs you.

Theft sub-limits, soft costs of delay, hot work permits, and where the project hands off to permanent property decide what a builders risk claim pays. We read all of it with you before a loss, not after.

Builders Risk, The McDade Way

What a builders risk policy actually pays for is decided long before the loss. The theft sub-limits, the soft costs of delay, the hot work permit program, and the day the project hands off to permanent property coverage. We translate the contract before claim time, so a delay or a theft on site does not turn into a number you have to absorb.

What Builders Risk Actually Covers. Six clauses worth reading before groundbreaking.

Direct Physical Loss to the Building Under Construction

Fire, vandalism, wind, hail, lightning, theft of installed building components, water damage from non-flood sources, and most other direct physical loss perils. Coverage applies to the structure itself during the build. Once substantial completion occurs, standard Commercial Property typically takes over.

Materials and Supplies On Site

Materials and supplies at the construction site, plus materials in transit and at temporary storage locations. Critical because copper, lumber, HVAC, appliances, and jobsite equipment are frequent theft targets. Sub-limits for off-site storage and in-transit apply.

Soft Costs of Delay

Additional architectural fees, additional engineering fees, additional financing interest, additional legal fees, additional permit fees, and additional taxes incurred as a result of a covered loss delaying the project completion. Soft cost coverage is a separate sub-limit and is the most common missing endorsement on Texas Builders Risk policies.

Temporary Structures, Scaffolding, and Forms

Coverage for temporary structures, scaffolding, forms, fences, and related temporary construction equipment used in the project. Sub-limits apply. Off-site coverage typically requires a specific endorsement.

Replacement Cost Valuation

Most Texas Builders Risk policies value the loss on Replacement Cost basis rather than Actual Cash Value. Price escalation endorsements protect against material cost inflation beyond stated thresholds (typically 5 to 10 percent). With material costs rising materially since 2020, the escalation endorsement is now standard on most Texas projects.

Common Exclusions

Faulty workmanship, faulty design, faulty materials, ordinary wear and tear, mechanical breakdown, government action, war and terrorism (separate coverage available), nuclear hazards, employee dishonesty (Commercial Crime covers), and earth movement (typically requires endorsement). Texas-specific freeze exclusions emerged post-2021 Winter Storm Uri on many carriers and require evaluation.

Builders Risk Insurance Request

Texas Builders Risk has the most severe theft environment in the country. Plus statutory frameworks that change the contract structure.

Texas construction projects operate under the Texas Insurance Code, the Texas Property Code (mechanics liens and the Texas Trust Fund Act), the Texas Anti-Indemnity Act in construction contracts, and the highest construction theft rate in the United States. The Texas Department of Insurance regulates Builders Risk carriers in Texas.

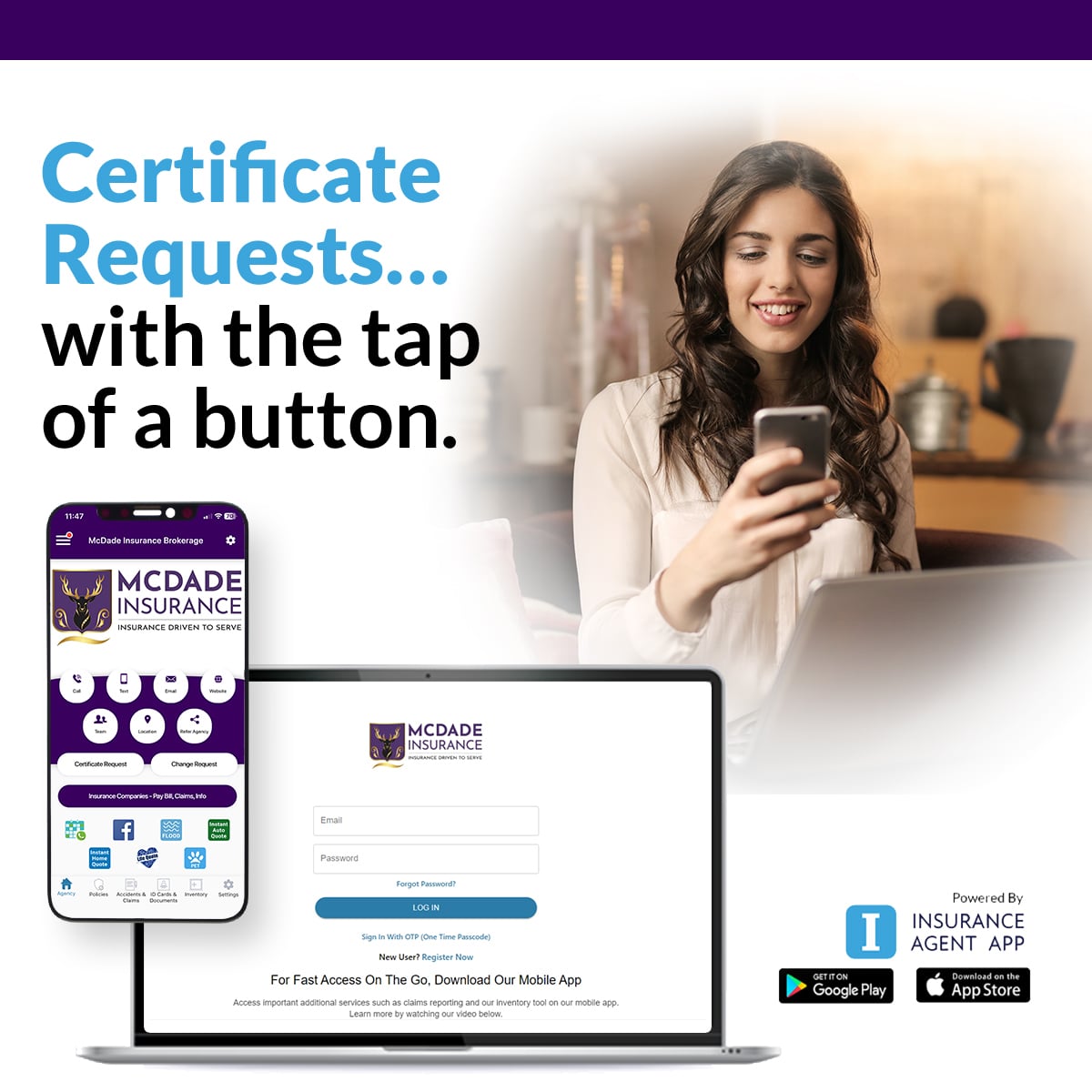

Your COIs. On Your Phone.

McDade clients get instant access to certificates of insurance from a mobile app. Issue. Email. Manage. No phone tag. No waiting on email.

Issue COIs on demand from your phone, anywhere, 24/7.

Email certificates directly to general contractors, vendors, or job sites in seconds.

Manage active certificates and policy info in one place.

Issue Certificates from your phone. The agency stays at the center.

If your business gets a certificate of insurance request twice a week, the McDade Client App removes that bottleneck. Pull an active certificate, edit the certificate holder, and email the COI to a general contractor, project owner, or job site directly from your phone in seconds. Free to McDade clients. SOC 2 Type II compliant.

Certificates on Demand

Issue COIs to general contractors and project owners in seconds.

Auto ID Cards

Current commercial auto ID cards on field employees' phones.

Mobile Claims Kit

Document construction site losses from the scene with photos.

Direct McDade Contact

Tap to call Dallas Downey or the McDade service team.

Built on the Insurance Agent App platform by GoInsuranceAgent, a Vertafore Orange Partner.

SOC 2 Type II compliantThis coverage sits in a portfolio. Here is what sits next to it.

Commercial Property

Standard Commercial Property covers the completed building. Builders Risk covers the building during construction. The two policies hand off at substantial completion. McDade coordinates the transition.

General Liability

Third-party bodily injury and property damage from construction operations. Often bundled into wrap-up (OCIP/CCIP) programs alongside Builders Risk on larger Texas projects.

Texas Surety Bonds

Performance and payment bonds required under Texas Government Code Chapter 2253 for public works projects exceeding statutory thresholds (25,000 dollars payment bond, 100,000 dollars performance bond).

Texas Workers Compensation

Texas Workers Compensation for construction employees. Texas is the only state where WC is optional, but most general contractors require WC certificates from subcontractors.

Texas Builders Risk Insurance. Read the questions worth asking.

What does Texas Builders Risk Insurance cover and what are the most common claim types?

Texas Builders Risk Insurance covers direct physical loss to the building under construction, materials and supplies on site or in transit, temporary structures and scaffolding, and soft costs of delay including additional architectural fees, additional financing interest, additional legal fees, and additional taxes. The Insurance Services Office Builders Risk Coverage Form (BR 00 06) is the standard foundation form. Coverage typically applies from groundbreaking through substantial completion. The most common Texas Builders Risk claim drivers are theft of materials (copper, lumber, HVAC units, appliances, electrical wire), fire from hot work activities (welding, cutting, brazing, soldering), water damage during the build (plumbing failures, weather, freeze during winter months), wind and hail damage to incomplete structures, and vandalism during off-hours.

Why is Texas the most severe state for construction theft?

Texas construction sites carry meaningful theft exposure for materials, tools, equipment, copper, HVAC, and appliances. The McDade Builders Risk Review evaluates theft coverage, sub-limits, off-site storage, in-transit coverage, security requirements, and how the policy transitions when the project reaches substantial completion.

What are soft costs and why does the soft costs endorsement matter?

Soft costs are the indirect expenses that accumulate when a covered loss delays project completion. Soft costs typically include additional architectural and engineering fees for revised plans, additional financing interest on construction loans extended beyond the original completion date, additional legal fees for permit re-applications and contract amendments, additional permit and inspection fees, additional taxes including property taxes accrued during the delay, additional advertising and marketing expense, and additional administrative cost. Soft costs are not covered by the standard Builders Risk Coverage Form unless specifically added by endorsement. Soft cost coverage carries a separate sub-limit. The soft costs endorsement is the most common missing endorsement on Texas Builders Risk policies. A 6-month delay on a Texas commercial project routinely produces 50,000 to 250,000 dollars in soft costs depending on project size.

How does the Texas Anti-Indemnity Act affect my Builders Risk program?

Texas Insurance Code Chapter 151, the Texas Anti-Indemnity Act, limits broad-form indemnification in construction contracts. A construction contract generally cannot require an indemnitor to defend or indemnify another party for that party's own negligence. The Act interacts with Builders Risk programs in several ways. Additional Insured endorsements on Builders Risk policies that would otherwise extend coverage to general contractors or project owners for their own negligence may be limited by Chapter 151. Wrap-up programs (OCIP and CCIP) require careful coordination with Chapter 151 because the wrap-up's combined coverage structure interacts with the indemnity language in subcontracts. The McDade Builders Risk Review evaluates the Anti-Indemnity Act exposure on each project.

What is a hot work exclusion and how do I protect against it?

A hot work exclusion or sub-limit applies to losses caused by welding, cutting, brazing, soldering, grinding, and other operations that produce heat, sparks, or flame. Hot work is one of the largest fire-loss drivers on Texas construction projects. Most Texas Builders Risk policies exclude or sub-limit hot work losses unless a documented Hot Work Permit Program is in place per NFPA 51B Standard for Fire Prevention During Welding, Cutting, and Other Hot Work. The permit program typically requires written authorization for each hot work operation, fire watch personnel during and after hot work, removal of combustibles from the work area, fire extinguishers available, and documented inspection. The McDade Review evaluates the hot work endorsement and the permit program implementation on each project.

What is a wrap-up program and when does it make sense for a Texas project?

A wrap-up program is a project-specific insurance program that bundles General Liability, Builders Risk, Workers Compensation, and Pollution Liability for the project across all enrolled contractors and subcontractors at the project. Owner-Controlled Insurance Programs (OCIP) are sponsored by the project owner. Contractor-Controlled Insurance Programs (CCIP) are sponsored by the general contractor. Wrap-up programs typically make sense for Texas projects exceeding 50,000,000 to 100,000,000 dollars in construction value, projects with high subcontractor counts (often 50 or more), and projects where the general contractor or owner can capture insurance cost savings through bulk purchase. Texas wrap-up programs require coordination with the Anti-Indemnity Act (Chapter 151), the Texas Trust Fund Act (Property Code Chapter 162), and Texas Workers Compensation subscription decisions.

How does Builders Risk transition to Commercial Property at project completion?

Builders Risk Insurance typically terminates at substantial completion (commissioning, certificate of occupancy, or owner acceptance, depending on policy language). At that point, standard Commercial Property coverage takes over for the building. The transition window matters significantly. A gap between Builders Risk termination and Commercial Property attachment exposes the building to loss with no coverage. An overlap creates redundant premium expense. The McDade Builders Risk Review coordinates the substantial completion definition in the Builders Risk policy with the inception date of the Commercial Property policy to ensure continuous coverage without gap and without redundancy.

What is a price escalation endorsement and do I need one?

A price escalation endorsement extends Builders Risk coverage to compensate for material and labor cost inflation between policy inception and the time of a covered loss. Without the endorsement, the policy pays based on cost at inception, which may fall short of actual replacement cost if material prices have risen meaningfully during the project. The endorsement typically activates above stated thresholds (5 to 10 percent inflation) and pays the inflated cost up to a stated limit. Given the material cost volatility since 2020 in Texas (lumber, copper, steel, concrete, glass, HVAC components), the price escalation endorsement is now standard on most McDade-reviewed Texas Builders Risk policies.

What is the McDade Texas Builders Risk Review?

The McDade Texas Builders Risk Review is an audit of your existing Builders Risk policy by Dallas Downey, CLCS, with the McDade commercial team. The review evaluates five primary areas. First, theft coverage and sub-limits against current Texas jobsite theft exposure. Second, soft costs coverage and limit against your project schedule and financial profile. Third, the hot work exclusion and the implementation of a Hot Work Permit Program per NFPA 51B. Fourth, the Texas Anti-Indemnity Act interaction with the Additional Insured endorsements on the policy and with the indemnity language in your construction contracts. Fifth, the transition coordination between Builders Risk substantial completion and Commercial Property inception. About 40 percent of the time the review confirms the current carrier and policy structure are correct. The other 60 percent identifies sub-limit, endorsement, or coordination opportunities.

Who handles Texas Builders Risk at McDade?

Dallas Downey, CLCS leads the McDade commercial insurance team including Texas Builders Risk. Dallas holds the Certified Lines Coverage Specialist designation and routes commercial conversations through a dedicated commercial meeting calendar. The McDade office serves the Houston metropolitan area including Spring, Klein, Tomball, Cypress, The Woodlands, Conroe, Humble, Katy, and Bridgeland, plus all of Texas through Premier Group Insurance carrier access including 50+ top Texas carriers we know well. McDade Insurance Brokerage Group is licensed by the Texas Department of Insurance (Texas License 2539471). Schedule a commercial review with Dallas through the commercial routing on this page or call the McDade office at 281.378.5002.

What Texas business owners say.

Real Google reviews from the Texas contractors, builders, and businesses the McDade team serves across Houston and the wider metro.

Send your current Builders Risk declarations. Dallas Downey audits all four.

The McDade Texas Builders Risk Review evaluates theft coverage and sub-limits against current Texas exposure, soft costs coverage and limit against your project schedule, the hot work exclusion and Hot Work Permit Program per NFPA 51B, and the Texas Anti-Indemnity Act interaction with Additional Insured endorsements and your construction contract indemnity language. Dallas Downey, CLCS leads the review. Most reviews complete inside one business week. About 40 percent of the time the audit confirms the current structure is correct. The other 60 percent identifies sub-limit, endorsement, or coordination opportunities.

Back to the commercial hub. Houston Business Insurance

Or call 281.378.5002

The review is advisory. McDade is licensed by the Texas Department of Insurance (Texas License 2539471).